You open your bank app, check your balance, and there it is a credit entry that reads something like “APBS CR ₹500” or “DBT/APBS Credit.” and now you’re wondering: “What on earth is APBS? Did I get this money by mistake? Is it legitimate?”

Don’t worry. You’re not alone.

Millions of Indians see this entry in their accounts and have no idea what it means. And honestly, the banking world loves throwing around acronyms without explaining them properly.

In this guide, we’ll break down everything you need to know about APBS – the full form, what it does, how it works step by step, and most importantly, what you should do if you’re not receiving your APBS payments.

Let’s get into it.

Also Read: How I Earn Money From Youtube

What is APBS? Full Form and Basic Meaning

APBS stands for Aadhaar Payment Bridge System.

APBS is a payment system that uses your Aadhaar number as an address to send government money directly into your bank account.

Think of it like this: your Aadhaar number acts like a “home address” for your money. When the government wants to send you a subsidy or benefit, they don’t need your account number or IFSC code anymore – they just need your Aadhaar. APBS does all the routing work behind the scenes.

| Term | Meaning |

| APBS | Aadhaar Payment Bridge System |

| Developed by | NPCI (National Payments Corporation of India) |

| Used for | Direct Benefit Transfers (DBT) by Government |

| Key identifier used | Your 12-digit Aadhaar number |

| Account type needed | Aadhaar Enabled Bank Account (AEBA) |

| Operated under | NACH (National Automated Clearing House) platform |

APBS in Banking – A Detailed Explanation

The Problem APBS Was Created to Solve

Before APBS, sending government money to crores of beneficiaries was a mess. Think cash disbursement through post offices, government agents, middlemen – and with that came delays, corruption, and money simply not reaching the right person.

The government knew they needed a smarter way. And that’s exactly when APBS came in.

APBS was built as part of India’s Direct Benefit Transfer (DBT) initiative, launched by the Government of India to cut out the middlemen completely and put money directly into people’s accounts.

What Exactly Is an Aadhaar Enabled Bank Account (AEBA)?

When you link your Aadhaar number to your bank account AND your bank updates this information in the NPCI Mapper, your account becomes an Aadhaar Enabled Bank Account (AEBA).

This is the account that receives APBS credits.

⚠️ Important Note: Simply linking your Aadhaar to your bank account is NOT enough. The bank must also seed (update) your Aadhaar into the NPCI Mapper. Only after this step does your account become eligible to receive DBT/APBS payments.

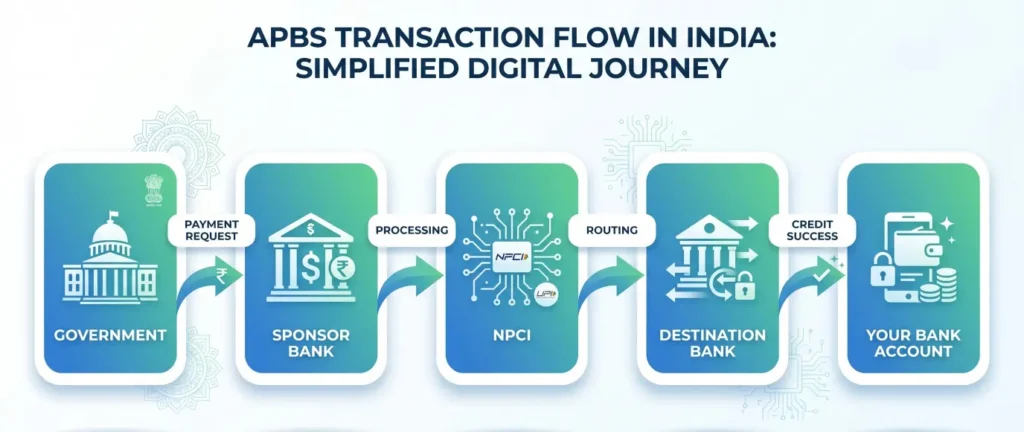

How APBS Works – Step by Step

Let’s say you’re eligible for the PM-KISAN scheme and ₹2,000 is being sent to you. Here’s exactly what happens:

Step 1: Government Prepares the Payment : The government’s ministry (say, Agriculture Ministry) creates a list of all eligible beneficiaries with their Aadhaar numbers.

Step 2: Sponsor Bank Submits to NPCI : This list goes to a Sponsor Bank (a bank that works with the government), which then submits the file to NPCI’s APBS system.

Step 3: NPCI Checks the Mapper : NPCI has a central database called the NPCI Mapper. It looks up your Aadhaar number and finds out which bank and account it is linked to.

Step 4: Money Gets Routed : NPCI routes the payment to your bank – called the Destination Bank – through the NACH platform.

Step 5: Your Account Gets Credited Your bank credits the amount to your Aadhaar-linked account. You get an SMS: “₹2,000 credited via APBS.”

Done. No paperwork. No travel to a government office. No middleman.

| Visual Flow of APBS Transaction Government/Ministry ↓ Sponsor Bank ↓ NPCI (checks NPCI Mapper using your Aadhaar) ↓ Destination Bank ↓ Your Aadhaar-Enabled Bank Account (AEBA) ✅ |

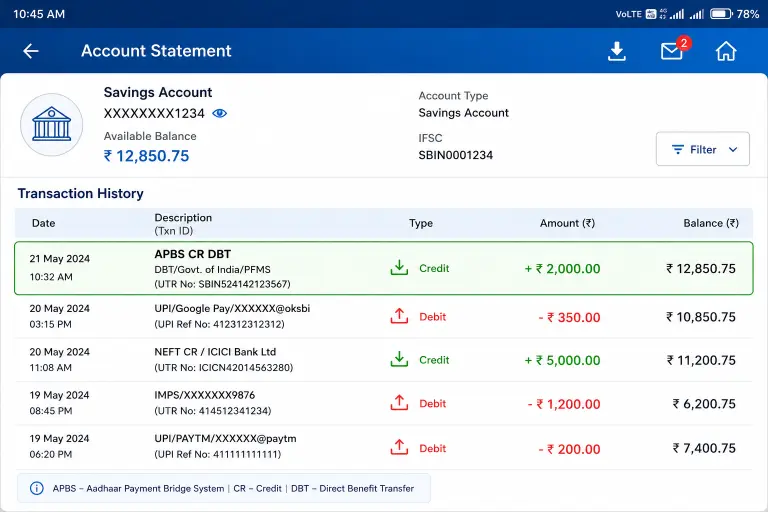

What Does “APBS Credit” Mean in Your Bank Statement?

When you see “APBS Credit” or “APBS CR” in your bank statement, it simply means:

“ A government scheme or department has transferred money directly into your Aadhaar-linked bank account using the Aadhaar Payment Bridge System.”

Common APBS Entry Formats in Bank Statements

| Statement Entry | What It Means |

| APBS CR | APBS Credit – money received |

| APBS/PFMS Credit | Payment via PFMS (Public Financial Management System) |

| DBT/APBS | Direct Benefit Transfer via APBS |

| APBS CR INW | Inward APBS credit |

| APBS – DBT | DBT scheme credited via APBS |

Example Bank Statement Entry:

| Date: 12-04-2026 | Description: APBS CR DBT PMKISAN | Amount: ₹2,000 CR |

This means PM-KISAN installment of ₹2,000 has been credited to your account.

Which Government Schemes Use APBS?

APBS is the backbone of India’s DBT (Direct Benefit Transfer) program. Here are the major schemes that use APBS to transfer money:

Central Government Schemes

- PM-KISAN – ₹6,000/year to farmers (₹2,000 per installment)

- MGNREGA – Daily wages for rural employment scheme

- LPG Subsidy (DBTL) – Pahal scheme for cooking gas subsidy

- PM Awas Yojana – Housing scheme payments

- National Social Assistance Program (NSAP) – Pension for elderly, widows, disabled

- Scholarships via NSP – National Scholarship Portal disbursements

State Government Schemes

- State-level pensions (old age, widow, disability)

- State scholarship programs

- Farmer input subsidy schemes

- COVID-19 relief payments

💡 Did you know? The APBS system is capable of handling 1 crore (10 million) transactions per day, making it one of the most powerful government payment infrastructure tools in the world.

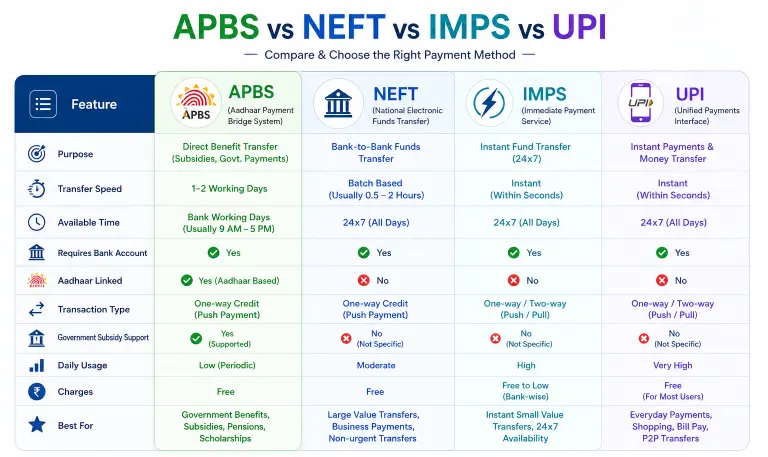

APBS vs NEFT vs IMPS vs UPI – What’s the Difference?

A lot of people confuse APBS with regular payment methods like NEFT or UPI. Here’s a clear comparison:

| Feature | APBS | NEFT | IMPS | UPI |

| Based On | Aadhaar Number | Account No. + IFSC | Account No. + IFSC | UPI ID / Mobile No. |

| Used For | Govt. DBT transfers only | General transfers | General transfers | All-purpose payments |

| Who Uses It | Government depts. | Individuals & businesses | Individuals & businesses | Individuals & businesses |

| Speed | Batch processed | Scheduled batches | Real-time | Real-time |

| Requires A/c details? | No – Aadhaar only | Yes | Yes | Yes |

| Available 24×7? | No (closed Sundays + RTGS holidays) | Yes (now 24×7) | Yes | Yes |

| For common people? | Recipient side only | Yes – send & receive | Yes | Yes |

Key Takeaway: APBS is not for personal transfers between individuals. It’s exclusively a government-to-citizen payment channel that uses Aadhaar as the routing key.

Benefits of APBS – Why It’s a Game Changer

1. No Middlemen, No Corruption

Money goes directly from the government to your account. No agent, no distributor, no local politician can intercept it.

2. One Account for All Schemes

You don’t need separate bank accounts for different welfare schemes. One Aadhaar-linked account = all benefits in one place.

3. Helps People in Remote Villages

Even someone in a village with limited banking access can receive money through a micro-ATM or Business Correspondent (BC) using their Aadhaar-linked account.

4. Transparent and Traceable

Every APBS transaction is recorded digitally. Governments, banks, and beneficiaries can all track payment status.

5. Faster Than Old Methods

No waiting weeks for a cheque or a money order. APBS payments are processed in batch sessions multiple times a day.

6. Cost-Effective

The government saves crores by eliminating cash handling, printing, and distribution costs.

Challenges and Limitations of APBS

APBS is great, but it’s not perfect. Here are some real challenges:

1. Aadhaar Seeding Errors

If your Aadhaar is linked to a wrong or closed bank account, payments will fail or go to the wrong place.

2. Multiple Account Seeding Problem

If you’ve seeded your Aadhaar with multiple banks, only the last updated bank in the NPCI Mapper will receive payments. This confuses many people.

3. APBS Not Available on Sundays

The system doesn’t operate on Sundays and on RTGS holidays declared by the RBI. So don’t expect transfers on those days.

4. Privacy Concerns

Since transactions are Aadhaar-linked, some people have concerns about biometric and financial data security. Though NPCI encrypts everything, it remains a valid public concern.

5. Exclusion of Non-Aadhaar Holders

People without Aadhaar cards – elderly people, migrants, those with documentation issues – can miss out on benefits.

Pros and Cons Summary

| ✅ Pros | ❌ Cons |

| Direct money to your account | Aadhaar seeding errors cause failures |

| No middlemen or corruption | Not available on Sundays/RTGS holidays |

| One account for all schemes | Multiple seedings cause confusion |

| Works in rural areas too | Privacy and data security concerns |

| Fully digital and traceable | Non-Aadhaar holders can’t access |

| Government saves costs | Requires active, correct NPCI Mapper entry |

How to Link Your Aadhaar to Your Bank Account for APBS

If you’re not receiving your government benefits, the first thing to check is whether your Aadhaar is properly seeded with your bank account in the NPCI Mapper.

Method 1: Visit Your Bank Branch

- Carry your Aadhaar card (original + photocopy)

- Fill the Aadhaar seeding/linking form

- Submit it at the bank counter

- Bank will verify and seed your Aadhaar in the NPCI system within 3–5 working days

Method 2: Net Banking / Mobile App

- Log in to your bank’s net banking or app

- Go to “Link Aadhaar” or “DBT Registration” section

- Enter your 12-digit Aadhaar number

- Verify via OTP (sent to your Aadhaar-linked mobile)

- Done – it gets updated in the NPCI Mapper

Method 3: ATM

Some banks (like SBI, PNB) allow Aadhaar linking via ATM using your debit card.

Method 4: Common Service Centre (CSC)

You can visit your nearest CSC or Jan Seva Kendra to link Aadhaar if you don’t have easy bank access.

How to Check Your NPCI Mapper / Aadhaar Seeding Status

Many people wonder: “Is my Aadhaar actually linked to the right bank for DBT?”

Here’s how to check:

- Visit https://resident.uidai.gov.in

- Look for “Aadhaar Bank Link Status” or “DBT Status”

- Enter your Aadhaar number + OTP verification

- You’ll see which bank account your Aadhaar is currently mapped to for DBT

You can also check on scheme-specific portals like:

- PM-KISAN Portal → pmkisan.gov.in

- NSP Portal → scholarships.gov.in

PFMS Portal → pfms.nic.in → “Know Your Payments”

Common Mistakes People Make with APBS (And How to Avoid Them)

❌ Mistake 1: Seeding Aadhaar in Multiple Banks

If you’ve opened accounts in different banks and seeded Aadhaar in all of them, only the last one in the NPCI Mapper gets the money. Keep only ONE active seeding.

❌ Mistake 2: Changing Bank Without Updating Aadhaar Seeding

Moved to a new bank? Opened a Jan Dhan account? If your old account is closed but Aadhaar is still seeded there, your DBT payments will fail. Always update the NPCI Mapper when you switch banks.

❌ Mistake 3: Thinking “Aadhaar linked to bank” = “DBT registered”

Linking Aadhaar to your bank is different from seeding it in the NPCI Mapper for DBT. Both steps must happen. Confirm with your bank specifically.

❌ Mistake 4: Ignoring Failed APBS SMS

If you get an SMS saying “APBS transaction failed,” don’t ignore it. Visit your bank immediately to check the mapper status.

❌ Mistake 5: Inactive Account

If your bank account has been dormant (no transactions for a long period), APBS credits may fail. Keep your account active.

Expert Tips for Smooth APBS / DBT Payments

💡 Tip 1: Always verify your NPCI Mapper status after opening a new account or changing banks. Don’t assume it’s automatic.

💡 Tip 2: Keep your mobile number updated in both your Aadhaar and bank account to receive instant SMS alerts for APBS credits.

💡 Tip 3: Check your passbook or bank statement at least once a month. Don’t let unclaimed credits sit in your account unnoticed.

💡 Tip 4: If your scheme money is not coming, check the scheme’s official portal first – sometimes the issue is with scheme eligibility, not APBS.

💡 Tip 5: For rural residents – AEPS (Aadhaar Enabled Payment System) lets you withdraw your APBS-credited money from a micro-ATM using just your fingerprint, even without a debit card.

APBS and Financial Inclusion in India

APBS is not just a technical payment system – it’s a social infrastructure tool.

India has more than 50 crore Jan Dhan accounts. Many of these belong to first-time bank users in rural areas who never interacted with the formal banking system. APBS became the reason they opened bank accounts in the first place – to receive government benefits.

This system has:

- Helped save over ₹2.7 lakh crore in reduced leakages and corruption (as per DBT Mission data)

- Supported payment of MGNREGA wages to crores of daily workers

- Enabled LPG subsidy to reach women directly under Ujjwala Yojana

- Made student scholarships reach beneficiaries without any agent

That’s the real power of APBS – it’s not just a banking acronym. It’s a financial lifeline for millions.

Frequently Asked Questions (FAQ) – APBS Full Form in Banking

APBS full form is Aadhaar Payment Bridge System. It is developed by NPCI and used to transfer government subsidies and welfare benefits directly into Aadhaar-linked bank accounts.

An APBS credit entry in your bank statement means that a government scheme or department has transferred money directly into your Aadhaar-linked bank account. It could be a subsidy, scholarship, pension, or welfare payment.

Yes, APBS credit is 100% legitimate. It is a government-authorized payment system operated by NPCI (which also runs UPI). If you see APBS credit, it’s real money from a genuine government scheme.

APBS is managed by NPCI (National Payments Corporation of India), which also manages UPI, IMPS, NACH, and RuPay. It operates under the regulatory oversight of the Reserve Bank of India (RBI).

No. APBS is an Aadhaar-based system. Without a valid Aadhaar number seeded with your bank account in the NPCI Mapper, you cannot receive APBS payments.

No. APBS operates on the NACH platform and remains closed on Sundays and RBI-declared RTGS holidays. Payments are not processed on these days.

If your APBS Aadhaar seeding points to a closed or inactive account, your payments will fail. You must visit your new/current bank and update the Aadhaar seeding in the NPCI Mapper immediately.

APBS (Aadhaar Payment Bridge System) is used by the government to send money to citizens. AEPS (Aadhaar Enabled Payment System) is used by citizens to withdraw or use that money using their Aadhaar fingerprint at micro-ATMs. Both use Aadhaar but serve different purposes.

So next time you see “APBS Credit” in your bank statement, you’ll know exactly what it is – not a mysterious entry, not an error, but a direct, transparent payment from the Government of India to your account.

APBS is genuinely one of India’s most impactful digital financial innovations. It’s quietly running in the background, making sure millions of farmers, pensioners, students, and families receive what the government promised them – without delays, without middlemen, without corruption.

If you’re a beneficiary of any government scheme, the single most important thing you can do right now is: verify your Aadhaar seeding status with your bank and in the NPCI Mapper. That one step ensures your money reaches you every single time.

📌 Take Action Now:

- Visit your bank branch or net banking to confirm your Aadhaar is seeded for DBT

- Check your scheme status on the official portal (PM-KISAN, NSP, PFMS)

- Keep your mobile number updated in your Aadhaar and bank account